The Numbers that Matter in 2026

The new year ushers in a wave of new limits that could influence your financial strategy.

Savers maximizing their employer retirement plan contributions will see a new change if they are 50 years old or older. Starting this year, if your wages exceeded $150,000 in 2025, the catch-up portion will be made as a Roth contribution. This will limit the pre-tax deductions to only the $24,500 limit, which would result in a meaningful tax change when compared to 2025.

For those who itemize deductions, 2026 brings new hurdles to charitable giving. A 0.50% Adjusted Gross Income (AGI) floor now applies, meaning only contributions above that threshold qualify for a deduction. For example, with an AGI of $100,000, the first $500 of donations will not count. You can only deduct amounts beyond that. High earners in the 37% tax bracket face additional restrictions, further limiting the value of itemized deductions.

Taxpayers using the standard deduction will now benefit from charitable donations made via check or credit card. If filing single, up to $1,000 of donations are deductible. For joint filers, the cap is $2,000.

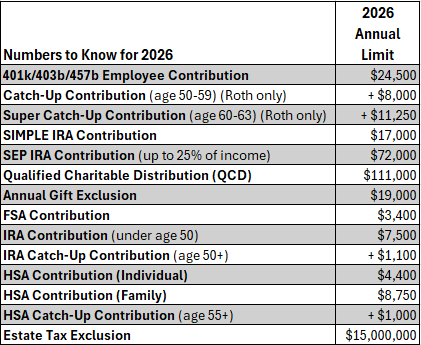

Almost every contribution threshold increased, so most people will feel the impact regardless of their planning goal. Take a look at the noteworthy changes for 2026:

Retirement Contributions:

- 401(k) Contribution Limit: $24,500

- 401(k) Contribution with Catch-Up (if you’re 50 or older): $32,500

- 401(k) Contribution with Super Catchup (only for ages 60-63): $35,750 (this is the ‘super catch-up’ contribution for those closer to retirement)

- IRA and Roth IRA Contribution Limit: Increased to $7,500 (subject to income limitations, but a Backdoor Roth IRA could apply)

- IRA and Roth IRA Catch-Up Contribution Limit (Age 50+): $1,100

Health Savings Accounts (HSAs):

- HSA Contribution Limit (Individual): $4,400

- HSA Contribution Limit (Family): $8,750

- Additional HSA Catch-Up (if you’re 55 or older): $1,000

Flexible Spending Accounts (FSAs):

- FSA Contribution Limit: $3,400

Charitable Giving:

- Qualified Charitable Distribution (QCD) Limit: Now $111,000 (a significant increase for those looking to donate directly from their retirement accounts)

- Standard Deduction to Exceed to Potentially Benefit from a Charitable Gift:

- $16,100 for Single Filers

- $32,200 for Joint Filers

Estate and Gift Planning:

- Annual Gift Tax Exclusion: $19,000 per person

- Estate Tax Exclusion: $15,000,000 per estate

Social Security:

- Social Security Cost-of-Living Adjustment (COLA) for 2026 benefits: 2.8%

Now is a great time to review your financial plan and make adjustments where needed. Higher contribution limits create opportunities to save more for retirement and healthcare, while new charitable giving rules may require a shift in strategy to maximize deductions. Whether you’re focused on tax efficiency, estate planning, or simply staying ahead of inflation, understanding these changes will help you start 2026 on the right foot. Wondering whether these updates should change your financial strategy? Contact us today.

< Back to Insights