What Are Trump Accounts? Should You Use Them?

Starting July 4th, 2026, the Trump Account, a new type of federally backed savings vehicle, will become available for children. In short, they are designed to accumulate assets for a child’s future with flexible contribution sources and IRA-like tax treatment. Let’s dive into the most important components.

Who is Eligible and How Do I Open One?

Any child under the age of 18 with U.S. citizenship and a Social Security Number is eligible. Only one account is allowed per child. To request an account, simply visit the Trump Account website and click the “Get Started” button. Check with your tax preparer to see if they already helped you file this form on your 2025 tax return. The account will be custodied at a U.S. Treasury-selected institution, but you should have the option to transfer the account to another institution if desired.

Contribution Capability

The investments in the Trump Account are restricted to US stock index funds. These will be interesting accounts as various types of depositors are permitted to contribute:

- Individuals (parents, grandparents, etc.) can contribute an aggregate of $5,000 per year.

- Tax treatment: Individuals do not receive a tax deduction for their contributions, but the income and growth within the Trump Account grows tax deferred.

- Employers can contribute up to $2,500 per year. If an employer contributes any amount, the $5,000 Individual cap is reduced dollar for dollar. Many Fortune 500 companies have already pledged to contribute to their employees’ children.

- Tax treatment: Employer contributions will count as a tax-deductible business expense.

- The U.S. Treasury is providing a free, one-time contribution of $1,000 for any child born between January 1, 2025, and December 31, 2028. This $1,000 doesn’t reduce the $5,000 Individual cap.

- Charities can elect to contribute an unlimited amount to any individual Trump Account. If your child was under the age of 10 in 2025, the Michael & Susan Dell Foundation has committed to contribute $250, if the child lives in a U.S. ZIP code with a median income of no more than $150,000. These charitable contributions also do not reduce the $5,000 Individual cap.

Distribution Rules

Earnings will be taxed as Ordinary Income. If funds are distributed before the child reaches age 59 ½, a 10% early withdrawal penalty will also apply unless an exception exists. For example, up to $10,000 can be used to purchase a first home. Moreover, the funds can be used penalty free if used for qualified higher education expenses.

Is a Trump Account a good fit for my child or loved one?

If the child is eligible for free contributions from the U.S. Treasury, Dell Foundation, or potentially your employer, then it’s at least worth opening the account. This will allow the free money to potentially grow into a nice nest egg for the child’s future.

It’s an easy decision to accept free money, but a whole other decision to put your own hard-earned resources into it.

Trump Account or UTMA?

If we look at Trump Accounts purely from an income tax perspective, an UTMA (custodial) account will likely beat the Trump Account for most people. An UTMA account has the advantage of tax free investment income (up to certain “kiddie tax” limits).

With that said, UTMAs are not eligible for free contributions from the federal government. Moreover, a Trump Account is also eligible for a Roth Conversion once the child turns 18, which provides several advantages. A Roth Conversion is a taxable event, so it’s important to work with a financial planner or tax professional as you consider this concept.

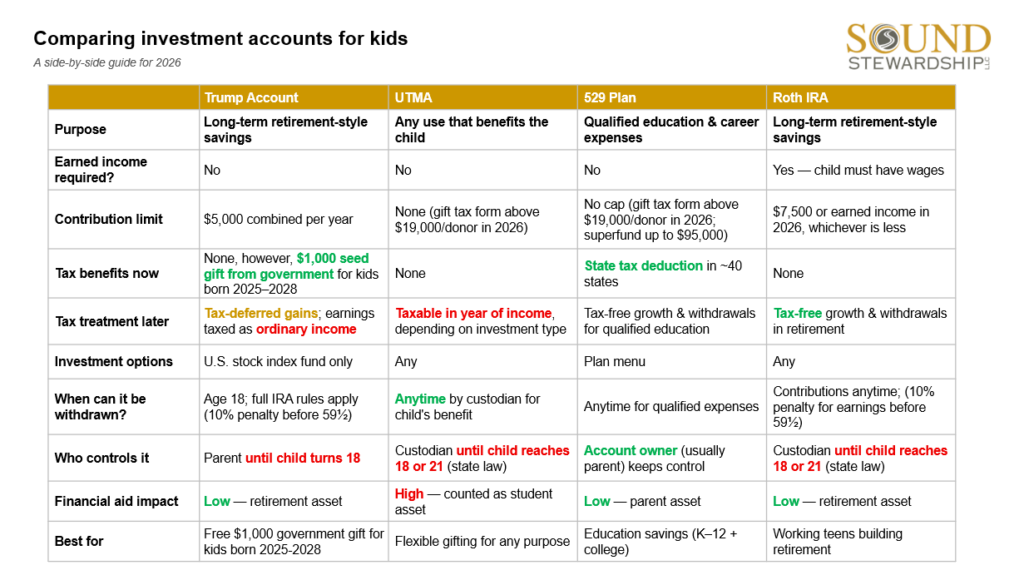

Everyone’s situation is unique, so deciding to contribute depends on your personal goals. To assist, we have created this chart that highlights the differences between available accounts for children

Trump Account vs. UTMA vs. 529 Plan vs. Roth IRA

We also offer a video that walks through the pros and cons of each option in more detail. If you would like personalized guidance, we invite you to schedule a meeting with a Sound Stewardship advisor to determine the best approach for your loved one.