How to invest this election year

The last couple years of market swings (significantly down in 2022 then an upbeat rebound in 2023) has left many investors feeling confused. In our climate of global & political turmoil, the prospect of an election only adds to the uncertainty.

Election years sometimes make even the most seasoned investors uneasy. Markets can react to political events, creating fluctuations that may leave portfolios in flux. The natural inclination might be to adopt a wait-and-see approach, but short-term knee-jerk reactions rarely lead to long-term favorable outcomes.

Studies have shown there’s little correlation between election outcomes and market performance. Regardless of which party is in power, people (and the companies they work for) continue living their lives to the best of their ability, adapting to whatever changes the government enacts. Yet our politicians and these election outcomes trigger intense feeling.

Regardless of your political persuasion (our firm serves all kinds), the public discourse includes more anger, anxiety, frustration, and doubt than usual. In such an election year, what should be done with our personal finances?

Strong emotion is not usually the friend of wise investment decisions, so great caution is advised. If you’re feeling worried, it’s worth stepping back to gain some perspective. This is true any time, not just because we’re in the middle of an election. If you’re second-guessing your investments now, it’s time to second-guess your investment philosophy overall.

Below are four principles of investing which are true anytime — including election years:

Note: These timely reminders were first posted during the 2016 election. It turns out they still apply!

1. Investing is a long-term strategy.

Investing – specifically ownership in companies providing value to their customers and society as a whole – is the basis for wealth creation. This growth takes time, however, and though the long-term trend for markets is historically positive, markets rise and fall based on short-term risk factors. Because stock ownership has been good over long periods, but volatile for most short periods, investing should generally be done with a mindset of 10+ years out.

Investors aren’t usually good at keeping this mentality. Over the last 10 years, the average investor has experienced an annual return of 6%, even though their investment funds actually returned 7.7% annually over that same period. Why the disparity? The gap between these two is a result of investors making investment decisions based on emotion and buying or selling at the wrong time.

Source: Morningstar’s “Mind the Gap 2023” Investor Report

2. Your investments should reflect your personal plan.

If you’re worried that money you need soon will lose value in a market crash, that money shouldn’t be invested in the first place. Investing is a long-term strategy. It should only be undertaken with long-term dollars.

This mismatch of investments with time horizon is a common mistake I see investors make. Those who need their money soon subject it to too much market volatility. Those who are saving for 30 years from now are too worried about short-term issues.

For instance, if your investments are primarily designated for your daughter’s college education expenses and she starts her freshman year in the fall, then you shouldn’t subject your money to the risk (or even potential return) of the market at all.

If you are a retiree who needs to live off your portfolio for an unknown period of time, your time horizon is different. You have both short-term needs (groceries over the next couple years) and long-term needs (groceries 10 years from now). Your short-term money still shouldn’t be put at risk. You can still take a long-term approach, however, by making sure you have built up cash reserves for up to 3 years’ worth of expenses that will make weathering most market cycles possible.

In either case, your approach would be much different from an endowment fund such as Harvard’s, whose time horizon is essentially perpetual.

3. No one can predict the future.

Why is it impossible to predict the market? The market’s position today is an indication of what investors expect the future holds. So the market’s position six months from now will be based on the outlook investors see from that future date. In other words, predicting the market is not just about trying to predict the future – it’s trying to predict what the future believes about the future!

I cannot tell you what expectations will be in the world after the election (although I could make some plausible sounding stuff up), and I certainly cannot tell you what expectations will be in 2034 for long-term investors.

“Forecasts may tell you a great deal about the forecaster;

they tell you nothing about the future.”

~Warren Buffett

Here’s what I do know: Uncertainty is a constant in the economy. Every decade has its own list of threats, and the news thrives off bombarding us with the crises du jour. We consistently go through cycles of expansion and contraction on a regular basis. Although we may know where we are in a market cycle, we cannot know how long a bull run or bear market will last.

No one can predict the future. But you CAN be prepared. Because the market is cyclical, switching from extremes of greed and fear, it should come as no surprise that the market will have regular setbacks.

4. Investment decisions should be led by principles, not emotions.

Ultimately, since market timing doesn’t work, true investing must be done based on principles. Any other approach leads to emotional decision-making that causes wild swings in the market in the first place.

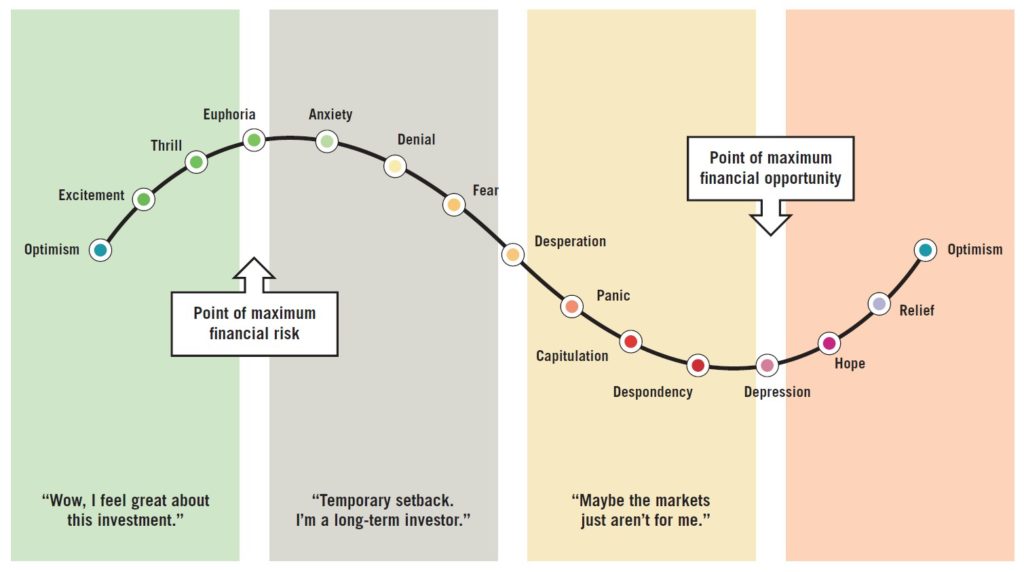

The typical emotion-based investor cycle:

What ultimately sets the best investors apart is that they take a disciplined approach to make sure their money matches their beliefs about how the economy works.

It’s easy to get caught up in the emotion of an election and let the temptation to react take over quickly. Leaders of our nation do set the direction for how the government will align or pull away from the principles you believe impact the economy. This can’t be ignored. But don’t let the short-term worry (how markets will react tomorrow) become more important than the long-term possibilities.

One final comment: wise King Solomon had a proverb, “The lazy person claims, ‘There’s a lion out there! If I go outside, I might be killed!’ ” (Proverbs 22:13). ). Sometimes it’s just easier to think about all the possible threats out there and do nothing. Are theoretical dangers keeping you from doing the right thing with your finances?

Or are you focusing on what you can control by living faithfully according to sound stewardship principles? These ancient principles work for any economic condition, at any level of net worth. That’s what we love about them.

Do you need your own personal investment plan based on timeless principles? Contact our Wealth Advisors today to schedule a consultation.

< Back to Insights